The Galleria-fication of Everything and the Armani Strategy

AI is bringing the Sherwin Rosen superstar effect to everything, but there is a response

The dominant story about AI is that it eliminates the work. The robots come, the jobs go, and the only question is how fast.

But that’s not what technology has actually done over the last forty years. Look at what happened to goods. There is Hermés and there is Temu. The pattern of a hollow middle is everywhere.

What’s really going on is more of an “average is over” story—but not in the way most people think.

Services have been mostly immune to this so far. That’s about to end. That’s what AI does that prior IT waves didn’t, and the firms that figure out how to respond have a 1981 fashion-industry playbook to learn from.

Production, Distribution, and the Real Superstar Effect

The cleanest explanation for this pattern starts with a 1981 paper by Sherwin Rosen called “The Economics of Superstars.” Rosen modeled why small differences in talent could produce enormous differences in income in a world where it costs nothing to serve one extra customer. The key mechanism was joint consumption: a performer’s output can be enjoyed by many people simultaneously, so the best performer doesn’t just capture a slightly larger audience—they capture the entire market.1

But Rosen’s model has only one knob: distribution costs. In real life, there are two. Technology can reduce the cost of production, or the cost of distribution, or both, and which costs fall determines what kind of market you end up with. The strongest bifurcation effects emerge only when both fall together.

This is what people miss when they hear “superstar.” They think it’s a story about the high end. It isn’t. High segmentation benefits the low end too. When technology drives down costs for budget options, the budget consumer gets a better deal than they had before. The market bifurcates into two viable positions, premium and budget, while the middle hollows out.

When you have real variation in both quality and cost, markets naturally produce a spectrum of options. The high-quality, high-cost product exists at one end. The low-quality, low-cost product exists at the other. And in between, you get a thick middle: products that are good enough and cheap enough to satisfy consumers who can’t afford the best but don’t want the worst.

This middle exists, in large part, because of search costs. When it’s expensive to find and compare alternatives—when you have to physically drive to stores, or rely on word of mouth, or trust whatever your local market happens to stock—the “good enough” option thrives. It survives not because it’s optimal for anyone, but because it’s the best option most people can find within their search budget.

Once the cost of searching goes down, this local optimum disappears. Consumers can now trivially compare the best with the cheapest and make a direct choice between the two. The middle, which never had a strong value proposition on either dimension — not the best quality, not the lowest price — gets squeezed from both sides.

This is exactly what the internet did to retail.

The poster child for the middle hollowing out is the Galleria. Gallerias were the canonical middle-class mall of the American 90s experience. Let’s go to the mall, indeed. In 2008, due to the recession and overleveraged real estate loans, malls started to go under. Combine this with the rise of the internet and a “retail apocalypse” was upon us. And yet.

High-end malls are doing better than ever. They attract high-income shoppers, who attract luxury stores, which supports higher rents, which creates a self-reinforcing cycle of accumulating value. Strip malls are doing great too—but for the opposite reason. They’ve gotten cheaper and cheaper, which has allowed them to proliferate. They cut costs faster than they lost revenue.

It’s why the Galleria—the middle-class mall, neither luxurious nor bargain-basement—died while Neiman Marcus and Dollar tree thrive.

Why Tech Ate the Middle (But Not Services)

We can see this pattern clearly in software. The internet decreased the cost of distribution for almost everything digital, which is why low-marginal-cost-to-serve businesses experienced winner-take-all effects. There is Smartsheet for enterprise and Monday.com for startups. But there is no middle-class task manager. The middle got killed because once distribution costs approach zero, consumers can see and choose between the best and the cheapest, and there’s no reason to settle for something in between because software has zero marginal cost.

The same bifurcation has played out across the economy in sectors where technology reduced both production and distribution costs simultaneously. We live in an economy driven by Rosen’s superstar effects, where even small changes in productivity yield very large differences in revenues.

But not everywhere.

In service industries, distribution costs fell but production costs didn’t. A doctor might be the best neurosurgeon in the country, and might even become famous for their skill, but they can’t turn that into superior distribution because the work must be done by them, in person, 12 hours a day. A partner at a law firm can attract more clients through online marketing, but they still can only work so many hours in a day. In all these cases, technology improved the marketing and delivery of the service, but it didn’t give leverage over production.2

And so prices for services simply went up. The famous price chart showing the sectors where costs have risen fastest—healthcare, education, legal services—has many lenses (most notably government regulation), but it is also a chart of services that have not been able to benefit from the collapse of production costs that digital and manufacturing technologies delivered elsewhere.

Junior employees in service industries primarily do rate-limiting work. It is bottleneck theory: there is work that must be done, either as a required step of the service or as a required part of a bundle demanded by the client, but it is too low-value to be done by the principal. The solution is to use lower-level labor. Junior employees are typically less skilled, so this also serves as a training ground. But the work is often less good, less consistent, less fast. Plus it requires hiring someone.

Everyone loves the story of the ATM and bank tellers, where bank tellers reskilled and automation meant that there were more bank tellers than before.3 At this point, it’s nearly canon. The problem with this story is that it’s sort of a lie. Yes, if you look at the Bureau of Labor Statistics, the number of people with the job “bank teller” was higher in 2010 than in 1970. But the job is fundamentally different. Bank tellers used to hand out cash. Today it is primarily a sales function that still does some vestigial banking work. It’s a different job, just with the same name.

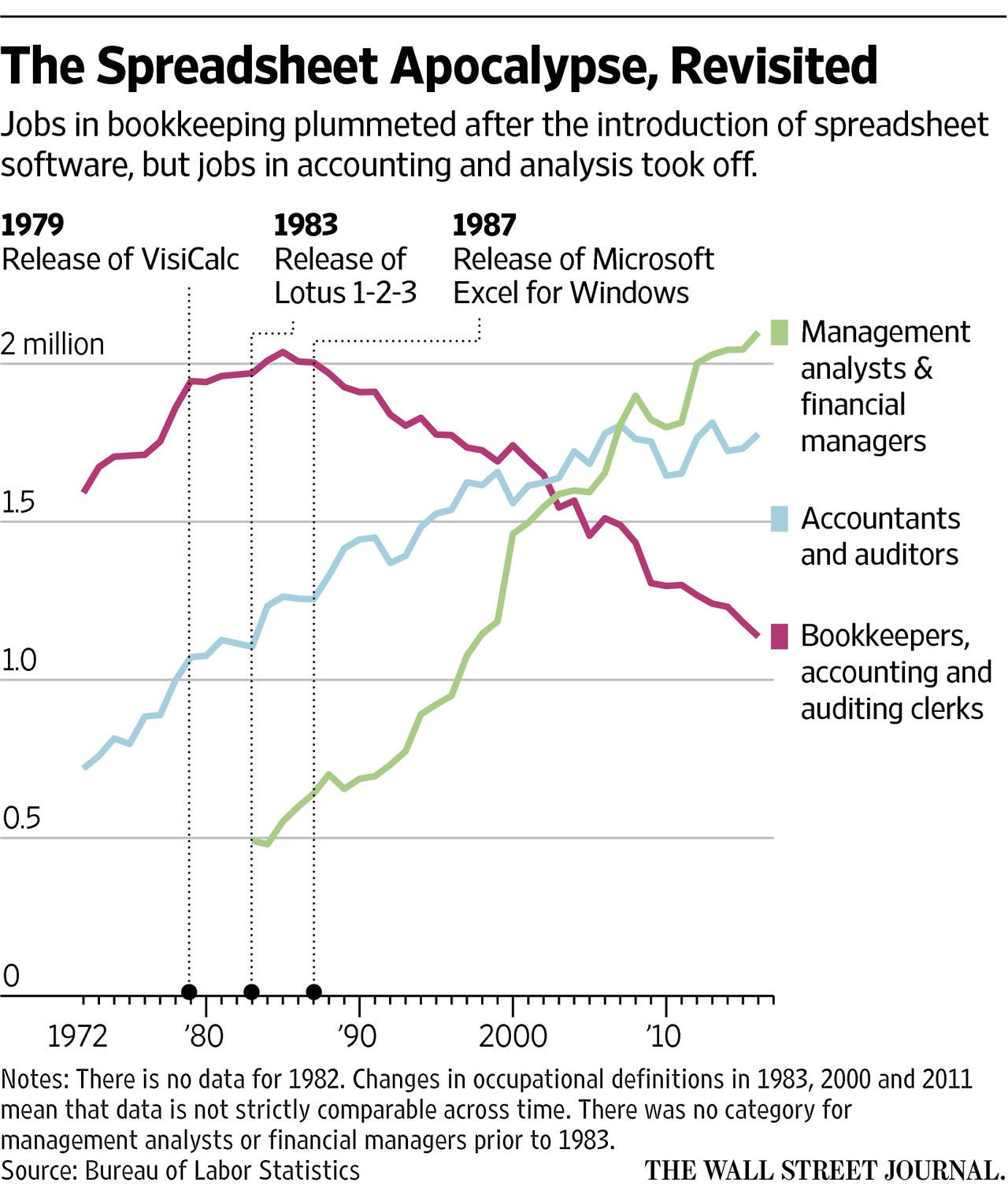

The story of accounting and bookkeeping is a more honest one. Before the introduction of bookkeeping, there were about 2 million bookkeepers and 1 million accountants and auditors, a 2-to-1 ratio. Although the number of bookkeepers increased slightly with the release of Visicalc, about a decade later, Microsoft Excel came out, diffusion increased, and bookkeepers went on an inexorable decline. Today there are only about 1.2 million bookkeepers, the same number of accountants 50 years ago despite a 50% population increase. But there are now nearly 2 million accountants and even more financial managers, a job that didn’t even exist before the spreadsheet. On top of that, bookkeeping is now a more sophisticated profession, so they earn more.

AI is about to do to services what the spreadsheet did to bookkeeping, but more so. Every prior IT wave helped people do the work. LLMs do the work. That’s the structural break. Telemedicine, legal tech, document automation, and SaaS all promised to hollow out professional services and didn’t, because they collapsed distribution and gave practitioners better tools, but they left the actual production of expert judgment untouched. AI changes that. For the first time, services can experience the simultaneous collapse of production and distribution costs that creates true superstar dynamics.

This is the most exciting thing about AI. It gives leverage to services. And that means the Galleria-fication that already swept through retail, software, and manufacturing is coming to law, medicine, consulting, and every other professional service.

The Emporio Armani Strategy

So how do firms rejuvenate themselves with young talent?4 The answer, I am beginning to believe, lies with a pathbreaking fashion brand.

In 1981—the same year Rosen published his superstar paper—Giorgio Armani had a very innovative idea: what if the masses could buy Armani suits at non-Armani prices? Historically, luxury brands would never put their imprints on lower price points; too risky for the brand halo.5 Armani’s solution was to create a “diffusion” brand called Emporio Armani. “Armani” clearly indicated to customers that they were getting the brand’s unique styling and attention to quality. But “Emporio” clearly indicated that they weren’t getting the flagship tailored suit but rather a ready-to-wear option (for which they paid a premium relative to the segment). It was a gigantic hit that not only created a new category but also benefited the flagship brand by creating loyal customers who “upgraded” as they moved up the economic ladder.

The Emporio model shows the way forward for services. If the Galleria-fication of services is inevitable, then the question is: what happens to the associates, the junior professionals, the people who used to populate that middle?

They become the diffusion tier. Junior employees will manage their own clients, do jobs to completion, and work with them as they grow until they’re ready to “graduate” to do flagship work. Crucially, this also solves the apprenticeship problem that AI otherwise creates. The traditional path of juniors doing fragments of senior matters until they absorb the craft breaks down when AI does the fragments. The diffusion tier6 replaces it: juniors run whole matters earlier, at lower price points, for clients who couldn’t have afforded the firm at all before. The training ground moves from inside senior work to alongside it.

This works only because AI raises the floor for everyone, including junior employees. It’s the low-end benefit of high segmentation in action. AI doesn’t just make the best lawyers more productive — it makes junior lawyers good enough to run their own client relationships at a lower price point. The budget consumer gets access to credentialed, brand-backed legal services that didn’t exist before. The premium consumer gets more partner attention and AI-augmented sophistication. The middle — the general-practice firm that was neither elite nor cheap — is what disappears.

Obviously, this is great for consumers. Emporio Armani was better than a random no-name suit brand, and demand was instantly ravenous. The same will be true for diffusion service brands. A lot of the technology that powers this segmentation will also be great for new brands and ultra-boutique specialized practices. But it will be devastating for the middle. Mid-tier firms, like JC Penney, Gap, and other Galleria-like brands before them, will struggle to justify their existence.

We’ve seen Galleria-fication in most sectors of the economy. Services are now no longer immune. The economic questions are pretty well resolved. The social questions of what happens when there are no more Gallerias to run to are much less certain.

The general idea of compounding returns is now visible across the economy, in superstar cities and superstar firms, though most uses of “superstar” abuse the term. Rosen’s paper has a very specific mechanism and is about market share, not prices.

Rosen's original model assumed only distribution costs fell — that's where the classical superstar effect comes from, and it's what drives the increasing-returns dynamic in superstar cities. The argument here extends Rosen by adding production costs as a second axis. When distribution costs fall, but production hits a wall, you end up with increased demand without increased supply, just increasing prices.

Bank tellers have now finally started to decrease—30% since 2010—but it is because of the internet, not any kind of bank automation. Apps are just now a better sales channel than branches as people do more banking online.

The other big social question is what will happen to “get-by” jobs that people use to sustain themselves during hard times or when they’re just getting started. Many directors like Michael Bay made commercials before they made it big—does RunwayML mean the end of this low-stakes way for early career filmmakers to sustain their craft? Musicians like Jeff Beck got by doing session work and writing jingles before they became famous—does Suno end that path to breaking into the music industry? The question is less about how a young Conan O’Brien will survive. The issue is more that performing at Groundlings allows young talent to do local work in their craft to hone it and network.

Companies that licensed their names to downmarket products, like Christian Dior and Pierre Cardin, were viewed as devaluing their brands. The near-destruction of the Christian Dior brand through licensing coincidentally led to the creation of LVMH.

It is not particularly important whether the diffusion tier has its own brand. All that matters is that it is clearly marketed as a separate tier from the mothership, indicating some level of shared provenance.